The world air cargo market is heading in opposition to a ‘hot Q4’ of charge will enhance after a sixth straight month of double-digit whisper in June, with a warning that shippers and forwarders unwell-ready for this year’s top season might well presumably furthermore procure themselves ‘on the mercy of the market,’ in accordance with basically the most up-to-the-minute evaluation by Xeneta.

Attach a matter to in June, measured in chargeable weight, used to be +13% year-on-year, persevering with the upward pattern viewed staunch via the major half of 2024. In distinction, cargo offer grew at its slowest dash in 2024, edging up easiest +3% year-on-year.

READ: CALLS FOR LABOUR TO EASE BURDEN ON LOGISTICS SECTOR

Which skill that, the world air cargo dynamic load ingredient – Xeneta’s size of skill utilisation in retaining with volume and weight of cargo flown alongside readily in the market skill – increased by +4% pts year-on-year.

While June’s knowledge, alongside previous months of annual whisper, must be balanced in opposition to the broken-down comparison viewed in the corresponding months of 2023, market gamers are genuinely busy strategizing on the perfect solutions to navigate the monetary challenges and opportunities anticipated to brand themselves in Q4.

“June’s whisper in ask used to be no longer shocking and we’d demand to see a continuation of double-digit year-on-year whisper in July and August because of low ask in the same months final year. The world machine is humming along properly at this level – however here’s doubtless the restful earlier than the storm in phrases of air freight rates,” stated Niall van de Wouw, Chief Airfreight Officer at Xeneta. “I’ve heard already that obvious airlines and forwarders are thinking of enforcing a top season surcharge by the pause of August. There’s a consensus this could increasingly be a hot Q4 for air cargo in lots of Asian markets.

“We demand decrease ask whisper year-on-year in the second half of 2024 because of such a sturdy Q4 2023 comparison, however for those that haven’t organized your Q4 skill by now, that you simply will most certainly be in for reasonably a jog. Shippers can pay extra staunch via Q4, the ask is how well-known extra?” he added.

READ: AIR INDIA TO PROPEL MAJOR EXPANSION IN AIR CARGO OPERATIONS

Having a leer at ask vs. offer for the final quarter of 2024, van de Wouw stated ‘the principles of the sport are turning into certain’ and appreciate strict compliance stipulations. Shippers and forwarders with skill agreements in markets that are ‘tight’ already, in retaining with fixed volumes and a top surcharge, can appreciate reduced possibility, while those dependent of the distance market can demand to pay ‘a hefty premium’.

“In 2023, the market didn’t no longer sleep for the ask we seen. This year, it does. Shippers with skill agreements in build will most certainly be better ready, however if they bolt above the agreed upon threshold, they will face paying market rates. On the temporary space market, this might presumably mean +50% will enhance in rates above what we see now, as soon as the market genuinely heats up.

“Asset holders will most certainly be strategizing; how well-known skill they’d well aid in the abet of to sell at a premium when this happens. While you were in an airline’s footwear, you’d be obvious you had a accurate chunk of skill to sell on the premium susceptible to be paid on the temporary market,” van de Wouw acknowledged.

The e-commerce whisper, disruptions in ocean freight because of struggle in the Crimson Sea, and regular enhancements in world manufacturers’ actions were the three predominant pillars riding up world air cargo space rates in June. These registered their biggest amplify of the year to this level, climbing +17% year-on-year to USD 2.62 per kg.

Measured month-on-month, the air cargo space charge edged up +2% in June, as the +4% month-on-month whisper of cargo ask continued to outpace skill offer.

Zooming into the corridor level, Southeast Asia to Europe and the US markets seen the biggest cargo space charge will enhance in June, rising +14% versus May perhaps presumably well to USD 3.65 per kg and USD 5.32 per kg respectively. Northeast Asia to Europe and the US furthermore experienced modest space charge will enhance, up +5% to USD 4.26 per kg and +4% to USD 4.00 per kg.

Conversely, outbound China markets stalled as China to Europe and the US rates each and every dipped -1% to USD 4.09 per kg and USD 4.80 per kg respectively. The Europe to US space charge fell -4% to USD 1.69 per kg due to the enhance of abdominal skill from summer season passenger flights.

Having a leer forward, many market uncertainties remain. Essentially the most up-to-the-minute manufacturing Shopping Managers’ Index (PMI) reported manufacturing manufacturing grew at a slower dash in June, with its subindex of novel export orders exhibiting the major decline in three months. This coincides with aloof-soft retail gross sales volumes in the US and Europe, despite cooling inflation.

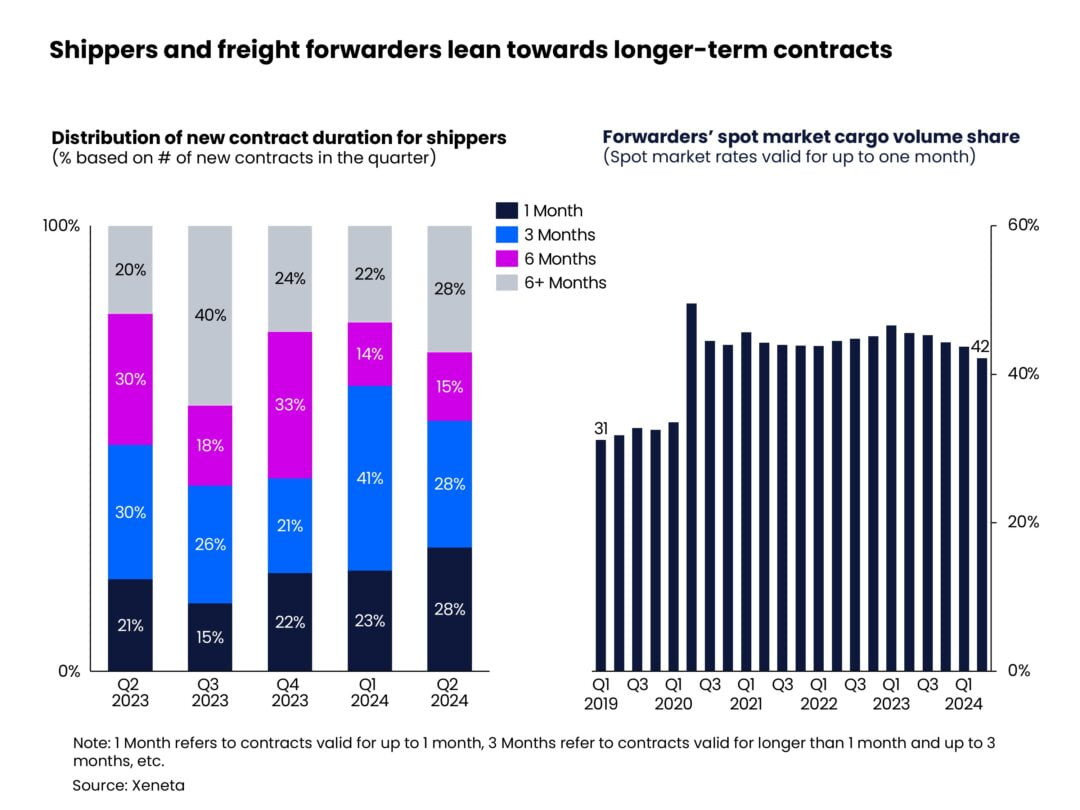

Given the market turbulence and the skill for an air cargo charge whisper in Q4, shippers are all over again adjusting their most well-most favorite contract lengths.

Within the second quarter of 2024, contracts lasting extra than six months topped the checklist, with an increasing fraction of 28%. Shippers are transferring in opposition to contracts of six months or extra to lead clear of the anticipated coarse freight charge fluctuations staunch via the upcoming year-pause top season.

The decrease in three-month contracts suggests unease among shippers about renegotiating rates accurate earlier than the year-pause top season.

Freight forwarders appear to fraction the same leer, furthermore procuring fewer cargo volumes in the distance market. Within the second quarter of 2024, the proportion of cargo volumes procured in the distance market accounted for 42% of the total market, exhibiting a -3% pts reduction versus a year ago.

“As we head into the second half of the year, it will most certainly be now or in no solution to remember longer-time interval contracts. With a combination of ocean transport chaos, an upturn in manufacturing actions, and dread-of-missing-out, a beautiful balance of rapid and lengthy-time interval contracts is on everybody’s thoughts. Most efficient time will narrate, however no subject happens, you’re going to be paying plenty extra to ship items from Asia Pacific as soon as September comes,” van de Wouw stated.